Adyen’s 2Q25 Credibility Test: When a Guidance Cut Meets Margin Expansion

A 2% headwind, €185 rebound, and the clearest proof yet that Adyen’s “single platform” thesis is more than engineering perfectionism — it’s strategic advantage in action.

TL;DR:

The Guidance Paradox: While cutting growth guidance, Adyen expanded EBITDA margins to 50% and maintained medium-term targets — signaling operational control and platform economics at work.

Platform Signals: New disclosure focus on billion-euro platform customers, 68% adoption of Uplift’s Protect module, and doubling embedded finance users shows a shift from payment processor to financial infrastructure.

Credibility & Control: Quantifying headwinds as a 2% impact for “a handful of customers” turned panic into nearly €185 rebound, proving that clarity and architecture-driven agility can move markets as much as results.

From WSJ: Adyen’s Earnings before interest, taxes, depreciation, and amortization for the first half of the year was 543.7 million euros, up 28% on year but missing market consensus by around 1%. The Ebitda margin landed at 50%, compared with 46% for the same period a year earlier.

I've been tracking Adyen for three years, and this quarter represents the clearest test yet of whether their "single platform" thesis creates genuine strategic advantages or just operational efficiency. The market's schizophrenic reaction - panic followed by recovery - suggests most investors are still missing the platform transformation story that's been building for eight quarters.

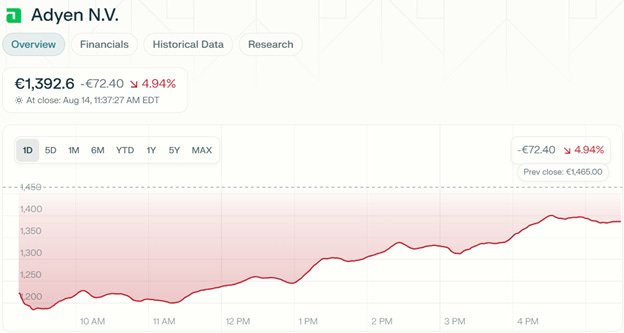

The conventional narrative around Q2 was simple: macro headwinds hit, growth guidance cut, time to sell. But something fascinating happened during the earnings call that revealed how little this narrative captured about Adyen's actual business evolution. When CFO Ethan Tandowsky quantified the guidance impact as "approximately 2% higher growth if you take this subset of customers out," the stock began a remarkable intraday recovery that ultimately reclaimed €185 per share.

This wasn't just about reassuring investors on the scale of tariff impacts. It was about demonstrating the analytical precision and strategic control that separates infrastructure companies from those merely riding cyclical trends.

The Metrics Detective Work: What Adyen Chooses to Emphasize

The most revealing aspect of any earnings report isn't what companies say - it's what they choose to measure. Adyen's Q2 metrics evolution tells a story of deliberate strategic repositioning that began in Q1 2025.

New Metrics Introduced (Strategic Priority Signals):

"Platform customers processing >€1B" - First quantified in Q1 2025 (30), now 32 in Q2

"Business customers on Platforms" - 193K vs 104K H1 2024 (+85%)

"Issuing volume >€2B" - First disclosed as specific figure in Q2 2025

"68% enterprise adoption of Protect module" - Granular product adoption metric

Metrics They're Downplaying:

Total processed volume - Mentioned +5% but quickly pivoted to "+23% ex-large customer"

Geographic revenue breakdown - Less emphasis on APAC challenges despite being primary headwind

Employee headcount growth - De-emphasized after previous quarters of hiring focus

This shift reveals something profound: Adyen is training investors to focus on platform monetization rather than volume growth. The introduction of granular product adoption rates (68% Protect adoption) signals genuine confidence in value-added services expansion, not just payment processing scale.

Consider this management quote from the call: "Two-thirds of our customers in the first half that started with us have implemented Protect from the beginning." This isn't a typical payment processor metric - it's a platform company talking about day-one product adoption rates.

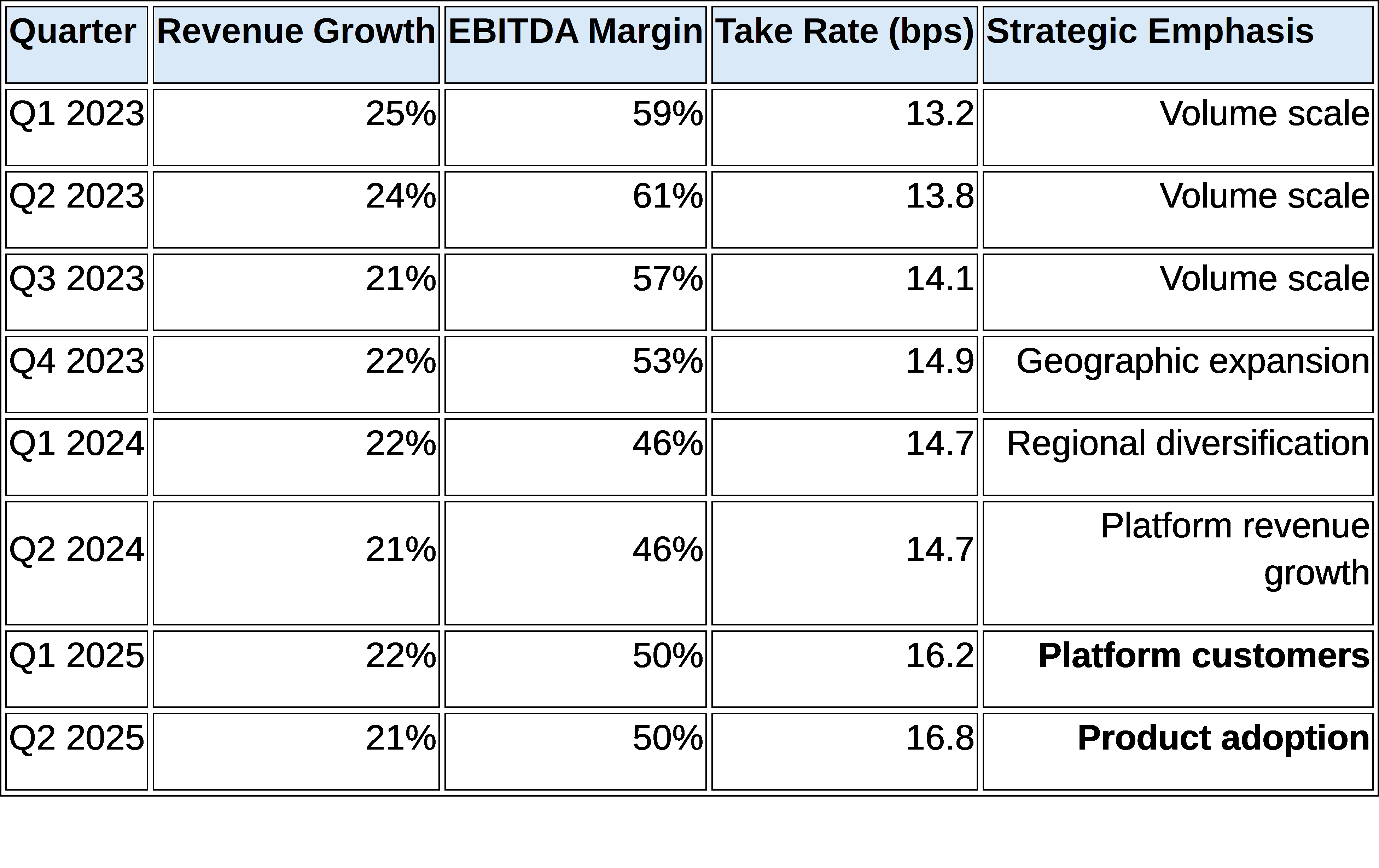

Historical Pattern Recognition: The Eight-Quarter Platform Build

Product adoption

The pattern is unmistakable: Q1 2025 marks the inflection point when Adyen began reporting platform-specific metrics, signaling transformation from payment processor to platform infrastructure provider. More importantly, the take rate progression from 14.7 bps to 16.8 bps over 12 months indicates pricing power expansion, not commoditization pressure.

This matters because it contradicts the prevailing narrative about payment processing becoming commoditized. Adyen's increasing take rates suggest they're moving up the value chain successfully, extracting more revenue per transaction through optimization services rather than competing on price.

The EBITDA margin recovery from 46% (H1 2024) to 50% (H1 2025) while maintaining 21% growth provides additional evidence of platform economics emerging. Traditional payment processors face margin pressure during growth investments; platform companies achieve operating leverage.

Technical Architecture as Competitive Advantage

Adyen's "single platform" approach has always sounded like engineering perfectionism rather than business strategy. Q2 2025 provided the clearest evidence yet that this architectural decision creates genuine competitive advantages.

The Strategic Agility Test: When APAC customers faced US tariff headwinds, management explained their response capability: "It's a single platform. It's a single integration. So it can be done in a couple of months to get up and running."

This seemingly technical detail reveals everything about competitive positioning. While competitors built through acquisition - creating systems that require months of custom integration for geographic expansion - Adyen's unified architecture enables strategic pivoting within quarters. When CFO Tandowsky noted they're helping affected customers expand into Brazil and Mexico, he wasn't describing a lengthy integration project but rather configuration changes.

Platform vs. Product Assessment:

The network effects evidence is becoming undeniable:

Data advantage: €1.3T annual processing volume improving machine learning models

Product stickiness: 68% Protect adoption among new enterprise customers

Platform momentum: 32 customers processing >€1B annually (vs 22 in H1 2024)

But the most compelling indicator comes from embedded finance scaling. Issuing volume exceeded €2B with customer count nearly doubling year-over-year. As management noted about their working capital product: "80% of users return for multiple loans."

This isn't payment processing anymore - it's financial infrastructure provision. The progression from payments to business accounts to working capital to issuing represents classic platform evolution: start with essential service, add complementary services, create switching costs through service integration.

Management Credibility Under Strategic Pressure

Adyen management has been notably conservative with guidance historically, making the Q2 "acceleration unlikely" change significant. However, the specific quantification approach suggests analytical rigor rather than broad uncertainty.

Guidance Evolution:

H2 2024: "Slight acceleration" in FY 2025 growth

Q1 2025: Maintained acceleration expectation with macro uncertainty caveat

Q2 2025: "Acceleration unlikely" with specific attribution to "handful of customers"

The credibility test came during Q&A when multiple analysts pressed for quantification. Tandowsky's response was precise: "You would take this subset of customers out, our growth would have been approximately 2% higher in Q2."

This level of analytical granularity during a guidance cut demonstrates operational control. Most companies cutting guidance provide vague macro explanations; Adyen quantified specific customer impacts and provided forward assumptions.

More importantly, they maintained medium-term targets despite near-term headwinds. The >50% EBITDA margin target for 2026 remains unchanged, suggesting confidence in platform economics despite growth rate moderation.

Strategic Messaging Consistency:

Co-CEO Ingo Uytdehaage's commentary remained focused on platform capabilities rather than quarterly results: "We want to take full control over the infrastructure... Because we have these licenses, we are capable of doing this. We have direct access to the clearing."

This infrastructure control theme has been consistent across multiple quarters, indicating genuine strategic conviction rather than quarterly positioning.

The Counter-Narrative: Why Recovery During Guidance Cut?

The market's initial reaction seemed logical: guidance cut equals negative sentiment. But the intraday recovery during the earnings call revealed something more interesting about investor understanding of platform businesses.

Popular Narrative: Adyen hit macro headwinds, growth slowing, margins under pressure.

Counter-Evidence from Q2:

EBITDA margin: 50% (vs 49.6% consensus) - expanding, not contracting

Customer acquisition: 2025 cohort growth rate exceeding platform average

Product innovation: 68% adoption rates showing premium pricing power

Take rate: 16.8 bps (vs 14.7 bps H1 2024) - monetization improving, not deteriorating

The disconnect between guidance (growth rate concern) and operational metrics (platform strength) created the recovery opportunity. As management detailed platform customer growth and product adoption rates, investors began recognizing that the growth quality was improving even as growth rate moderated.

Management's Platform Confidence: "The 2025 cohort so far is far outpacing where we were in the past couple of years... it's growing at a faster rate than the overall platform."

This statement during a quarter where they cut growth guidance reveals management's confidence in customer acquisition capability. They're not losing competitiveness; they're gaining customers faster while some existing customers face temporary headwinds.

The embedded finance momentum provides additional counter-narrative evidence. When management noted issuing customers "nearly doubling" year-over-year with >€2B volume, it became clear that platform transformation was accelerating despite macro challenges.

Competitive Positioning Through Infrastructure Control

Adyen's Q2 results illuminate how architectural decisions made years ago now determine competitive outcomes in volatile environments.

vs. Traditional Payment Processors:

Most payment companies built through acquisition, creating integration complexity that becomes strategic liability during disruption. When customers need rapid geographic pivoting (as with tariff impacts), acquired-and-integrated architectures require lengthy custom development.

Adyen's unified platform enables what management calls geographic agility: "We are active in the markets that we're looking for... It's a single platform. It's a single integration."

This architectural advantage compounds during uncertain periods when customers consolidate toward more capable providers.

vs. Platform Companies:

Unlike marketplace platforms that facilitate transactions between third parties, Adyen owns the infrastructure itself. This creates revenue predictability (processing fees vs. take rates on transaction volume) and direct customer relationships rather than ecosystem dependency.

The Q2 validation came through direct customer metrics: 32 platforms processing >€1B annually, with business customer count reaching 193K (+85% YoY). These aren't marketplace participants but direct platform customers building on Adyen's infrastructure.

Geographic Infrastructure as Moat:

Adyen's expansion strategy prioritizes local infrastructure depth over rapid market entry. Their Brazil operations demonstrate this approach: direct Pix integration, local acquiring licenses, and dedicated product development (Recurring Pix, Pix via Open Finance).

When tariff-affected customers needed geographic alternatives, Adyen's Brazilian infrastructure became competitive advantage. As management noted: "One of the markets that is looked into is both Brazil and Mexico to see how customers can further grow there. And we are active there."

This infrastructure-first approach creates switching costs through regulatory compliance and local optimization rather than just contractual lock-in.

Platform Innovation as Strategic Defense

The most interesting competitive development in Q2 was Adyen Uplift's enterprise adoption rate. Achieving 68% adoption among new customers for optimization software indicates genuine value creation rather than bundling tactics.

The Innovation Platform Effect:

Adyen Uplift represents platform evolution beyond infrastructure provision toward intelligence services. The product uses Adyen's €1.3T annual transaction data to optimize conversion, reduce fraud, and lower costs for customers.

Nord Security's results provide specific evidence: 10% conversion increase, 41% fraud reduction, 35% reduction in manual risk rules. This isn't marginal improvement but operational transformation.

Monetization Strategy Evolution:

Management's approach to Uplift pricing reveals platform thinking: "We are partly charging for it, so it depends a bit on the module that you're exactly using, and some of the parts are free... where we bring value to our customers, we will charge for it."

This value-based pricing approach differs from traditional software licensing or payment processing fees. Adyen charges based on customer outcomes rather than usage metrics, indicating confidence in value delivery.

The 68% enterprise adoption rate suggests customers recognize this value immediately rather than requiring extensive sales cycles.

Strategic Implications: Infrastructure During Disruption

Adyen's Q2 results reveal something important about platform businesses during uncertain periods: infrastructure advantages accelerate rather than diminish during disruption.

Customer Consolidation Dynamics:

When customers face external pressures (like tariffs), they consolidate toward providers offering strategic agility rather than just operational efficiency. Adyen's ability to facilitate geographic pivoting within months rather than quarters becomes competitive differentiation.

Management's confidence in customer acquisition despite macro headwinds suggests this consolidation is occurring: "The 2025 cohort so far is far outpacing where we were in the past couple of years."

Platform Economics Under Pressure:

Traditional businesses face margin pressure during growth investments or market uncertainty. Platform businesses with genuine network effects often achieve improved economics during disruption as customers increase engagement and adopt additional services.

Adyen's EBITDA margin expansion (46% → 50%) while maintaining growth during macro uncertainty provides evidence of platform economics rather than cyclical business characteristics.

Innovation Velocity as Defense:

The rapid scaling of Adyen Uplift (68% enterprise adoption) demonstrates how platform companies can accelerate innovation during market uncertainty. Infrastructure control enables rapid product development and deployment without integration dependencies.

This innovation velocity becomes self-reinforcing: better products attract better customers, more customers provide more data, better data enables better products.

What to Watch: Platform Maturation Indicators

Next Quarter Focus:

Platform customer progression: Targeting 35+ customers processing >€1B annually?

Product adoption scaling: Can Uplift maintain 60%+ enterprise adoption rates?

Geographic diversification: Evidence of tariff impact mitigation through market expansion?

Embedded finance monetization: Revenue contribution from issuing/working capital products?

Medium-Term Strategic Indicators:

Take rate sustainability: Can 16+ bps rates persist without customer pushback?

Platform network effects: Evidence of customer-to-customer referrals or ecosystem benefits?

Innovation pipeline: New products demonstrating platform data advantages?

Broader Industry Impact

Adyen's Q2 results suggest that in payment infrastructure, architectural decisions made 5-10 years ago are now determining competitive outcomes. Companies that built through acquisition are struggling with integration complexity while single-platform providers gain strategic agility advantages.

The earnings call recovery wasn't about quarterly results - it was about recognition that Adyen built the right architecture for an uncertain world. When guidance cuts coincide with margin expansion and customer acquisition acceleration, something interesting is happening beyond cyclical business dynamics.

The platform transformation that began appearing in Q1 2025 metrics isn't just operational improvement - it's competitive repositioning that may prove decisive as the industry continues consolidating toward infrastructure providers rather than transaction facilitators.

For investors willing to look beyond quarterly growth rates, Adyen's Q2 results provide evidence that infrastructure control creates genuine strategic advantages during uncertain periods. The market's intraday recovery during a guidance cut suggests growing recognition of this platform value, even if the full transformation remains underappreciated.

$ADYEN

General Disclaimer: The information presented in this communication reflects the views of the author and does not necessarily represent the views of any other individual or organization. It is provided for informational purposes only and should not be construed as investment advice, a recommendation, an offer to sell, or a solicitation to buy any securities or financial products.

While the information is believed to be obtained from reliable sources, its accuracy, completeness, or timeliness cannot be guaranteed. No representation or warranty, express or implied, is made regarding the fairness or reliability of the information presented. Any opinions or estimates are subject to change without notice.

Past performance is not a reliable indicator of future performance. All investments carry risk, including the potential loss of principal. This communication does not consider the specific investment objectives, financial situation, or particular needs of any individual.

The author and any associated parties disclaim any liability for any direct or consequential loss arising from the use of this material and undertake no obligation to update or revise it.